Investing in Rental Property vs. Notes in a Self-Directed IRA [CHECKLIST]

Rental property and private mortgages are some of the most popular investments for Self-Directed IRA and Solo 401(k) plans. As we speak with several hundreds of investors each month and participate in online investor forums, we are frequently asked which of the two is the better option. The reality is that there is no single right answer, other than maybe “both”. That said, we felt that outlining some of the key pros and cons of each approach would be a valuable exercise.

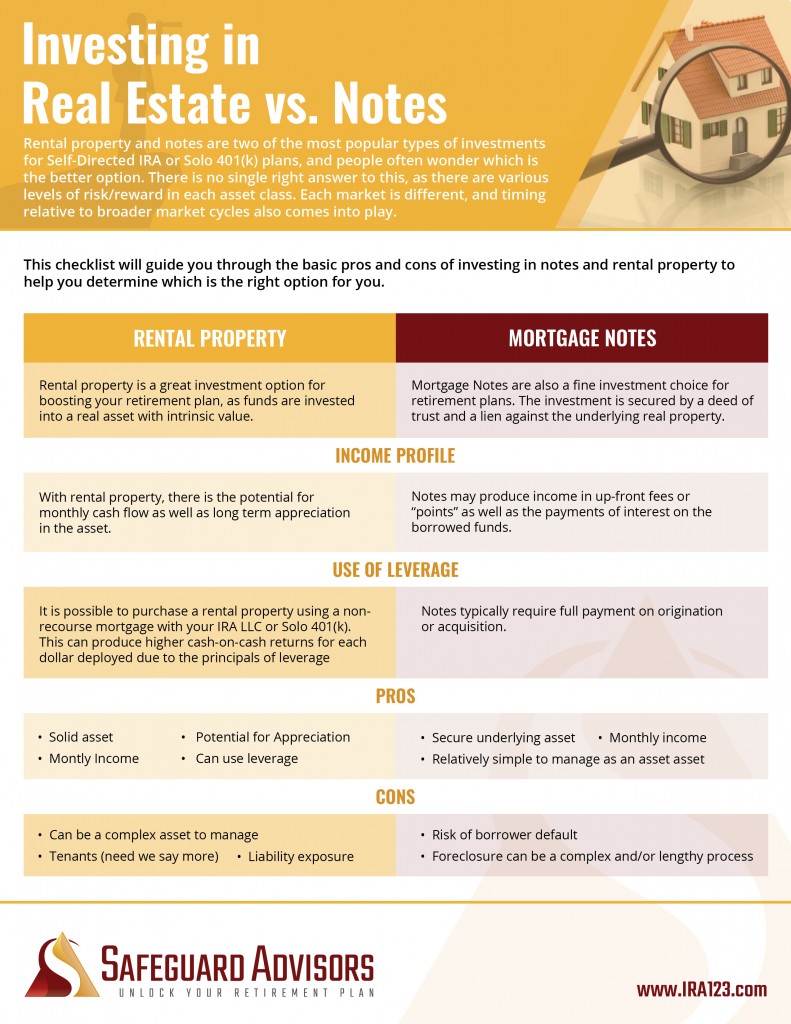

Investing in Rental Property

Rental property is a great asset for building retirement wealth. Your plan funds are invested into a real asset that has intrinsic value – providing a level of security not found in many asset classes. Real estate has the potential to create income both with monthly cash flow and appreciation in property value over time. One can also use mortgages to acquire real estate with an IRA or 401(k) plan and take advantage of the higher cash-on-cash returns that leverage provides.

Real estate is an asset class that most of us understand and are comfortable with. Many of our self-directed IRA investors have experience as landlords already. Understanding a particular real estate market and the potential and risks within that market, while somewhat complex and fluid, is a lot more linear than the multiple variables that can impact other investments such as equities. Real estate does go through cycles, but those cycles can be a lot easier to predict and do not come with the inherent volatility of financial markets. Being able to invest locally in an asset class you understand is a big plus.

On the down side, rental property requires tenants to pay the rent. Finding and retaining quality tenants requires skill, and a bit of luck thrown in. Managing tenants can be frustrating, and there is always the specter of damage to the property, vacancy between tenants, and even litigation. If you happen to have experience as a landlord, then being able to self-manage your properties. Otherwise, it may be best to hire a professional property manager. Either way, you have to put effort into the ongoing operating of a rental property investment to ensure the highest chances of success and profitability – either in managing tenants or managing the property manager.

Investing in Notes

Notes are also a type of investment that can produce excellent and consistent returns and boost the value of your tax-sheltered retirement savings. Notes come in many types, but the most common are those secured by real estate in the form of a deed of trust and mortgage. Like real estate, there is a solid asset underling the contract, but the enforceability and security of that asset can vary based on the note position as well as the loan to value (LTV) ratio between the note and the property. The higher the LTV, the greater the risk, especially if there is a drop in property values such that the property may be worth less than the outstanding loan.

Some notes hold a first position lien, while other notes can be in a 2nd or 3rd position subsequent to another note. These subordinate notes clearly come with additional risk. Such notes will typically offer a higher rate of return to offset that risk, but if the note defaults and you cannot buy out the preceding note holders, you may end up losing your investment in its entirety.

It is also possible to invest in non-performing notes, with the aim of resolving the issues and converting the note to performing status or taking control of the property. As with 2nd or 3rd position notes, this is a risk/reward decision for an investor. There is a potential for higher return, but with corresponding risk and/or legal complexity.

Most IRA note investors are focusing on less risky choices such as moderate LTV short term loans for fix and flip projects or moderate 3-5 year notes secured by performing properties.

Rates of Return

Whether rental property or a notes investment will produce better return is not always a simple question to answer, and will vary from market to market and by opportunity. As a general rule, it is somewhat easier to predict the return on investment for performing notes, as the interest rate is what it is. So long as the borrower makes the payments, that interest rate will be the return on investment. If you are investing in shorter term notes, you need to factor in the down time between one note paying off and being able to deploy the capital into another investment. Investing in notes that pay 12% return will only net you 10% annual return if the money is idle two months out of the year.

With rental property, you can make assumptions for operating expenses, unexpected repairs and vacancies, but you never really know from one year to the next exactly how close reality will match your projections. Likewise, appreciation is easy to predict in long cycles, but can be more variable over the short term. And that appreciation of the asset is only potential return up until the point you actually sell a property and lock in the gain.

Overall, you should expect similar average returns for a portfolio of relatively conservative performing notes compared to clean rental properties in a desirable neighborhood. In either class, you can change the risk reward levels, so when comparing options, be sure to consider where on the risk spectrum each choice may sit.

The Tax-Efficiency Myth

Many pundits in the real estate investing sphere promote the concept that they will only invest in notes with a self-directed IRA and not in rental property. The logic for this is that real estate can be very tax favored when done personally, and that one is giving up those tax-benefits when investing in real estate using a self-directed retirement plan. While that may be true, it is logic that entirely misses the point of investing IRA capital.

Do I care if I am foregoing tax benefits if my IRA is returning 13-15% returns each year while being deployed into a secure asset? The tax status of the IRA is what it is, and will always be different than the tax status of any investment made personally. The IRA money needs to be invested, and I want to find the best mix of security and consistent performance. If a rental property investment provides the best overall opportunity, then I will take that opportunity.

The tax efficiency issue may only come into play for an investor with significant personal holdings in real estate. In that case, it may make sense to focus the IRA on other investments such as notes, to create diversification. Put the tax-efficient asset on the taxable side of the equation and the notes inside the tax-sheltered vehicle.

Return on Investment is Always the Bottom Line

When it comes to evaluating whether to invest your IRA into notes or rental property, several individual factors will play into that decision. An investor who has experience in rental property and a proven business model (or contacts with providers of the same) will naturally lean towards putting their IRA to work in that fashion. Someone who is very busy, does not have expertise in landlording, or lives in a market where properties are too expensive and/or do not cash flow well may prefer notes.

All things being equal, one should evaluate the various rental property and lending opportunities available and see what option provides the best reward relative to the risk involved.

As I mentioned previously, sometimes the right answer is all of the above.

What our clients says about us

Quick answers to common questions

We’ll take you through a simple, step by step process designed to put your investment future into your own hands…immediately. Everything is handled on a turn-key basis. You take 100% control of your Retirement funds legally and without a taxable distribution.

YES! In 1974, Congress passed the Employee Retirement Income Security Act (ERISA) making IRA, 401(k) and other retirement plans possible. Only two types of investments are excluded under ERISA and IRS Codes: Life Insurance Contracts and Collectibles (art, jewelry, etc.). Everything else is fair game. IRS CodeSec. 401 IRC 408(a) (3)

It’s actually pretty simple. Early on, regulators let the securities industry take the lead in educating the public about retirement accounts. Naturally, brokers and banks promoted stocks, bonds, and mutual funds—giving the impression that those were the only allowed investments. That was never true... and still isn’t. You can probably guess why they kept the rest under wraps.

It is possible to use funds from most types of retirement accounts:

- Traditional IRA

- Roth IRA

- SEP IRA

- SIMPLE IRA

- Keogh

- 401(k)

- 403(b)

- Profit Sharing Plans

- Qualified Annuities

- Money Purchase Plans

- and many more.

It must be noted that most employer sponsored plans such as a 401(k) will not allow you to roll youraccount into a new Self-Directed IRA plan while you are still employed. However, some employers will allow you to roll a portion of your funds. The only way to be completely sure whether your funds are eligible for a rollover is by contacting your current 401(k) provider.

A Solo 401(k) requires a sponsoring employer in the format of an owner-only business. If you have a for-profit business activity – whether as your main income or as a side venture – and have no full-time employees other than potentially your spouse, your business may qualify. The business may be a sole-proprietorship, LLC, corporation or other entity type.

A self-directed retirement plan is a type of IRA or 401(k) that gives you greater control over how your retirement funds are invested. Unlike traditional accounts held at banks or brokerage firms that limit you to stocks, bonds, and mutual funds, self-directed plans allow you to invest in a wide range of alternative assets including real estate, private businesses, precious metals, cryptocurrency, and more.

These plans still follow the same IRS rules and maintain the same tax-deferred or tax-free benefits as conventional retirement accounts. The difference is simply in how and where you choose to invest.

No. Moving to a self-directed IRA or Solo 401(k) does not trigger any taxes, as long as your funds are eligible for rollover.

Self-directed retirement plans maintain the same tax-advantaged status as traditional plans offered by banks or brokerage firms. The key difference is flexibility—our plans are designed to give you greater control and allow for a wider range of alternative investments beyond stocks, bonds, and mutual funds.

A prohibited transaction is any action between your retirement plan and a disqualified person that violates IRS rules and can lead to serious tax consequences. Under IRS Code 4975(c)(1), prohibited transactions include:

- Selling or leasing property between your plan and a disqualified person Example: Your IRA cannot purchase a property you already own.

- Lending money or extending credit between the plan and a disqualified person Example: You cannot personally guarantee a loan your IRA uses to buy real estate.

- Providing goods or services between your plan and a disqualified person Example: You can’t use your personal furniture to furnish a rental property owned by your IRA.

- Using plan income or assets for the benefit of a disqualified person Example: Your IRA cannot buy a vacation home that you or your family use.

- Self-dealing by a fiduciary (using plan assets for their own benefit) Example: Your CPA shouldn't loan your IRA money if they’re advising the plan.

- Receiving personal benefit from a deal involving your IRA's assets Example: You can’t pay yourself from profits your IRA earns on a rental.

If a transaction doesn’t clearly fall within the allowed guidelines, the IRS or Department of Labor may review the situation to determine if it qualifies as a prohibited transaction.

Disqualified persons are individuals or entities that are prohibited from engaging in certain transactions with your IRA or 401(k). Doing so could trigger a prohibited transaction, which may result in taxes and penalties.

Here’s who is considered a disqualified person:

- You (the account holder)

- Your spouse

- Your parents, grandparents, and other ancestors

- Your children, grandchildren, and their spouses

- Any advisor or fiduciary to the plan

- Any business or entity owned 50% or more by you or another disqualified person, or where you have decision-making authority

These rules exist to prevent self-dealing and ensure your retirement plan remains in compliance with IRS regulations.

(Reference: IRC 4975)

Understanding and following these rules can be tricky, but it’s very doable. The best way to stay compliant is to work with professionals who specialize in self-directed retirement plans. They can help you navigate IRS guidelines and avoid prohibited transactions.

If an IRA holder is found to have engaged in a prohibited transaction with IRA funds, it will result in a distribution of the IRA. The taxes and penalties are severe and are applicable to all of the IRA’s assets on the first day of the year in which the prohibited transaction occurred.

Yes. While self-directed retirement plans allow for a wide range of investments, there are a few important restrictions.

You cannot invest in collectibles or life insurance contracts, and you must avoid prohibited transactions—activities that benefit you personally rather than the retirement plan. These include things like buying or selling property to yourself or family members, using plan assets for personal gain, or self-dealing in any way.

Violating these rules could cause your entire IRA to lose its tax-advantaged status. To protect your account, it’s essential to work with professionals who understand IRS regulations and can help you stay compliant.

This is a common misconception. In many cases, professionals may simply be unfamiliar with self-directed retirement plans, as they fall outside their usual scope of work. CPAs and tax preparers are trained to file taxes, not necessarily to advise on alternative retirement strategies. Financial advisors and brokers often work for firms that focus on traditional investments like stocks and mutual funds—and may not benefit from or support alternative options like real estate or private lending.

Self-directed retirement investing is legal under IRS rules—but like any specialized area, it requires working with professionals who understand how it works.

The IRS has rules in place to make sure your IRA is used only for the exclusive benefit of the retirement account—not for personal gain or to help family members. These rules can get complicated because there are many ways a conflict of interest can occur, even unintentionally.

For example, if your IRA buys a house and rents it to your mother, you might be reluctant to evict her if she stops paying rent. That emotional connection creates a conflict between what’s best for your IRA and your personal relationships, something the IRS aims to prevent.

These rules help ensure your retirement account stays compliant and protected. (See IRC 408)

Yes. Most tax-deferred retirement accounts—such as Traditional IRAs, old 401(k)s, 403(b)s, and TSPs—can be rolled over into a self-directed IRA or Solo 401(k), depending on your eligibility. Roth IRAs cannot be rolled into these accounts.

You can contribute directly from earned income, subject to annual IRS contribution limits. The method and amount depend on the type of plan you have (e.g., Solo 401(k) vs. IRA).

To take a distribution, you'll request funds through your custodian or plan administrator. Distributions may be taxable depending on your account type and age. Early withdrawals may be subject to penalties.

For 2025, the Solo 401(k) max contribution limit is $81,250 if age 60-63, $77,500 if age 50-59 or 69+, and $70,000 if under 50. Traditional and Roth IRAs have a limit of $7,000 ($8,000 if age 50+). Limits are subject to IRS adjustments.

Yes. IRA contributions are typically due by your personal tax filing deadline (e.g., April 15). Solo 401(k) contributions follow your business tax filing deadline, including extensions.

IRS reporting requirements vary depending on the type of self-directed retirement plan you have. Here’s a quick breakdown of what you need to know

Please note: Our team can help you understand what’s required for your specific account, but we don’t provide tax or legal advice. We always recommend working with a qualified tax professional to ensure full IRS compliance.

Self-Directed IRA (Traditional or Roth)

- Form 5498 – Filed by your custodian each year to report contributions, rollovers, and the fair market value (FMV) of your account.

- Form 1099-R – Issued if you take a distribution or move funds out of your IRA.

- Annual Valuation – You'll need to provide updated FMV for any alternative assets held in the account, such as real estate or private placements.

Solo 401(k)

- Form 5500-EZ – Required if your plan assets exceed $250,000 as of year-end. Must be filed annually by the plan participant.

- Form 1099-R – Required if you take a distribution or roll funds out of the plan.

- Contribution Tracking – Keep records of employee and employer contributions. These are not filed with the IRS but may be needed for tax reporting or audits.

SEP IRA

- Form 5498 – Filed by your custodian to report contributions and FMV.

- Form 1099-R – Filed by your custodian. Issued for any distributions.

- Employer Contributions – Must be reported on your business tax return (and on employee W-2s, if applicable).

Health Savings Account (HSA)

- Form 5498-SA – Filed by your HSA custodian to report contributions.

- Form 1099-SA – Filed by your HAS custodian. Issued for any distributions.

- Form 8889 – Must be included with your personal tax return to report contributions, distributions, and how funds were used.